$852 Billion and Rising: OpenAI’s $122B Raise Signals a New AI World Order

AI News | Editor: Sandy On March 31st 2026 OpenAI published an announcement of unusual weight: the company said it had completed its latest funding round, secur

AI News | Editor: Sandy On March 31st 2026 OpenAI published an announcement of unusual weight: the company said it had completed its latest funding round, secur

AI News | Editor: Sandy

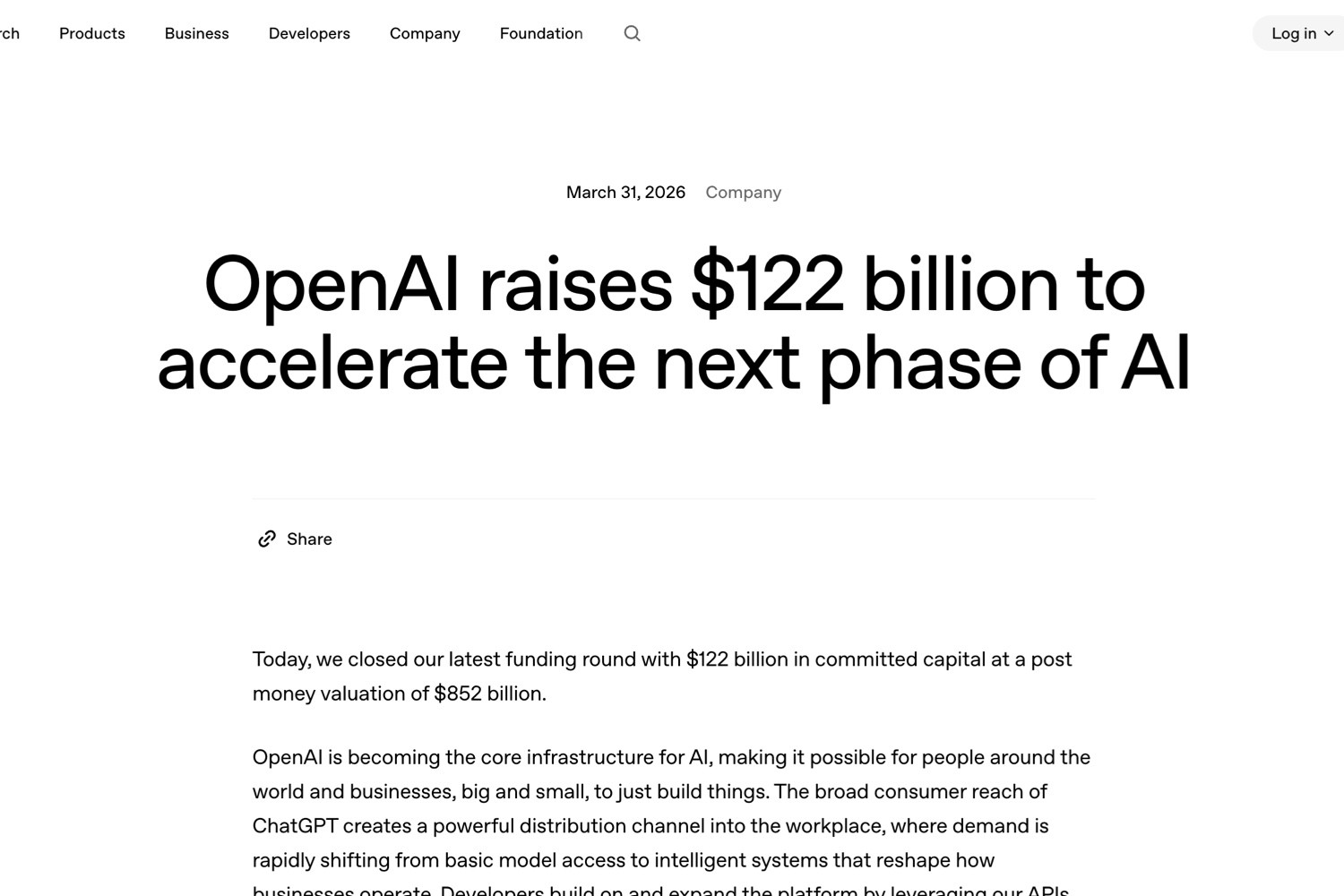

On March 31st 2026 OpenAI published an announcement of unusual weight: the company said it had completed its latest funding round, securing $122 billion in committed capital at a post-money valuation of $852 billion, with strategic backers including Amazon, NVIDIA and SoftBank, while Microsoft also remained involved. This is not merely one of the largest private funding rounds in history. More importantly, OpenAI has folded fundraising, infrastructure, product integration and a new route for retail investors into a single narrative. According to OpenAI’s official announcement, “OpenAI raises $122 billion to accelerate the next phase of AI” (https://openai.com/index/accelerating-the-next-phase-ai/), the money will be used directly to expand compute capacity, advance models and products, and speed up the commercialisation of what it calls the “next phase of AI”. If the market spent the past two years debating whether generative AI was a bubble or the start of a platform shift, OpenAI’s latest move looks more like a declaration that the main battleground has already changed: away from model capability alone, and towards whoever can most efficiently combine intelligence, compute and distribution into a vast and sustainable system.

Judging from the announcement, OpenAI does not present this round as a routine financial event. Instead, it frames it as a pivotal moment in the formation of AI infrastructure. The company says it is increasingly becoming core AI infrastructure, and argues that market demand is shifting from mere “access to models” towards intelligent systems that can genuinely reshape how businesses operate. That is a noticeable change in tone from earlier waves of AI hype. Previously, most companies launching models emphasised parameter counts, reasoning ability, benchmark scores or specific multimodal features. This time, OpenAI seems to be selling both capital markets and enterprise customers a broader proposition: what is truly valuable is not a single model, but the entire value chain running from chips, cloud and data centres to APIs, consumer products and enterprise workflows.

That also helps explain why the announcement specifically highlights multiple product lines including ChatGPT, the API business, enterprise tools, Codex, search, memory and multimodal interaction. OpenAI is clearly trying to tell the market that it is no longer simply the maker of a chatbot, but a company attempting to package AI as a general-purpose platform. That marks a subtle but important shift from how outsiders viewed OpenAI in 2023 and 2024. Back then, the core question was whether it could maintain its lead. Now the question is whether it can turn that lead into a form of infrastructural advantage that rivals will struggle to dislodge.

On the surface, the most eye-catching figures in the announcement are obviously the fundraising total and the valuation. But a closer reading suggests that the real technological signal lies in OpenAI’s emphasis on what might be called a “compute flywheel”. The company repeatedly argues that more compute leads to more intelligent models; better models then support better products; higher product adoption, in turn, drives revenue and cash flow, which can finance the next wave of compute investment. It is a characteristically Silicon Valley story of compounding returns, but it also captures the reality of frontier AI competition today: progress in models is no longer just a contest between research teams, but a broader competition involving supply chains, energy, cloud orchestration and product design.

OpenAI also unusually disclosed a more diversified infrastructure footprint, including cloud partners such as Microsoft, Oracle, AWS, CoreWeave and Google Cloud. On the chip side, beyond NVIDIA, it cited AMD, AWS Trainium, Cerebras and internally designed chips developed with Broadcom. That detail is particularly important. It suggests that while OpenAI still depends heavily on NVIDIA, it no longer wants its future tied entirely to a single hardware path. For a company whose growth remains closely constrained by GPU supply and the pace of data-centre construction, a multi-supplier strategy serves as risk management, a bargaining tool and perhaps a prerequisite for improving margins over time.

Another crucial phrase in the announcement is the idea of an “integrated AI super app”. At first glance, that sounds like the usual language of product marketing. In reality, it hints at OpenAI’s effort to redefine what ChatGPT is meant to be. It is no longer just an interface for answering questions. The company hopes to combine ChatGPT, Codex, browsing capabilities and fuller agentic functions into a unified entry point that can understand intent, execute tasks proactively, and move across different applications, data sources and workflows.

That product direction bears some structural resemblance to the “super app” concept long cultivated by Chinese internet companies. But OpenAI is not betting on a social graph or a payments network. It is betting on model capability itself becoming a new interface layer. If that strategy works, users may no longer need to switch constantly between search engines, office software, customer-service systems, programming tools and knowledge-management platforms. Instead, a single AI entry point could mediate far more activity across contexts. Seen through the lens of business models, this means OpenAI may be pursuing not just subscription revenue, but deeper control over workflows, along with future possibilities in transaction sharing, advertising, enterprise agency services and platform tolls.

According to Reuters’ report of March 26th 2026, “OpenAI's U.S. ad pilot exceeds $100 million in annualized revenue in six weeks” (https://www.reuters.com/business/media-telecom/openais-us-ad-pilot-exceeds-100-million-annualized-revenue-six-weeks-2026-03-26/), ChatGPT’s advertising pilot in the United States surpassed $100 million in annualised revenue within six weeks. That suggests the “super app” is not merely an abstract vision, but something that could gradually evolve into a more layered monetisation model. If search was the traffic gateway of the Google era, the AI assistant may become the next era’s allocator of attention. And once attention becomes concentrated, the methods of monetisation tend to multiply.

Viewed internationally, OpenAI’s trajectory represents a distinctly American model of AI development: vast capital, frontier models, immense cloud resources and strong product distribution are being used to expand rapidly and erect formidable barriers to entry. The contrast is already visible even within America itself. According to Reuters’ report of February 12th 2026, “Anthropic valued at $380 billion in latest funding round” (https://www.reuters.com/technology/anthropic-valued-380-billion-latest-funding-round-2026-02-12/), Anthropic’s latest valuation has reached $380 billion. And according to Reuters’ report of September 19th 2025, “xAI raises $10 billion at $200 billion valuation, CNBC reports” (https://www.reuters.com/business/xai-raises-10-billion-200-billion-valuation-cnbc-reports-2025-09-19/), xAI’s valuation has climbed to $200 billion. The three firms differ in strategy, but all point to the same reality: frontier AI has evolved from a start-up contest into a capital-intensive, infrastructure-intensive and energy-intensive industrial struggle.

China’s situation is different. According to Reuters’ report of February 12th 2026, “A year on from DeepSeek shock, get set for flurry of low-cost Chinese AI models” (https://www.reuters.com/world/china/year-deepseek-shock-get-set-flurry-low-cost-chinese-ai-models-2026-02-12/), after DeepSeek shook the market in 2025 with a low-cost model strategy, Chinese competitors began leaning more aggressively into open-source approaches and cost efficiency. In other words, American giants are competing to pile up the most compute, products and capital, while Chinese firms more often stress who can push models into wider deployment at lower cost. That does not necessarily make the Chinese route weaker. On the contrary, it may create a different kind of real-world competitive pressure, especially in price-sensitive markets and enterprise adoption.

Europe, meanwhile, is trying to carve out a third path. According to Reuters’ report of March 29th 2026, “France's Mistral raises $830 million in debt for AI data centre build-up” (https://www.reuters.com/business/finance/frances-mistral-raises-830-million-debt-ai-data-centre-build-up-2026-03-30/), France’s Mistral is raising money to build data centres and strengthen Europe’s autonomy in AI infrastructure. European firms may not be able to confront OpenAI head-on in terms of financial scale, but they can appeal to corporate customers uneasy about relying too heavily on American platforms, using arguments around data sovereignty, compliance, regional cloud capacity and open models. In that sense, the global AI race is no longer simply a contest over benchmark rankings. It is increasingly a competition between three institutional models: America’s platform capitalism, China’s cost-efficient ecosystem expansion, and Europe’s sovereignty- and compliance-driven approach.

The most important industrial significance of OpenAI’s announcement may not be the amount of money raised, but the way it describes AI as an “infrastructure layer” that requires sustained, capital-heavy investment over time. That framing is consistent with OpenAI’s earlier positioning around the Stargate project. According to OpenAI’s official announcement, “Announcing The Stargate Project” (https://openai.com/index/announcing-the-stargate-project/), the plan had already outlined an ambition to invest $500 billion over the coming years in AI infrastructure. This suggests that OpenAI is increasingly thinking like a cloud-computing giant: first secure capacity, then wrap it in products, and finally lock both the cost curve and the developer ecosystem into its platform.

Once AI is truly infrastructural, the competitive map of the industry will begin to change accordingly. First, the boundaries between model companies, cloud providers and chipmakers will become less distinct. Second, software firms may find their position in the value chain redrawn. In the past, SaaS companies built moats through interfaces and data flows. In the future, if AI agents can execute tasks directly across tools, the value of some intermediary layers may be eroded. Third, user behaviour may shift as well. As more people grow accustomed to using a single AI entry point to search, code, write, shop, handle paperwork and organise work, the central challenge for brands may move from “how to be seen” to “how to be selected by AI systems”.

None of this means the grand narrative is free of practical limits. The first is cost. Training, inference and global deployment for frontier models remain enormously expensive, while energy, data-centre capacity and chip supply cannot expand indefinitely. The second is regulation and geopolitics. AI infrastructure touches data governance, energy policy, export controls and national security. It cannot advance in a straight line purely at Silicon Valley speed. The third is uncertainty around monetisation. OpenAI has already demonstrated striking user and revenue growth, but whether such a lofty valuation can hold over time will depend on whether it can turn product stickiness into durable cash flow, rather than relying only on the market’s imagination about the future.

There is also a double edge to making OpenAI more accessible to ordinary investors. According to OpenAI’s announcement, the company will be added to several ARK Invest-managed ETFs. Investopedia noted in its April 1st 2026 report, “OpenAI Is Joining Cathie Wood's ARK ETF Lineup ...” (https://www.investopedia.com/openai-is-joining-cathie-wood-ark-etf-lineup-adding-new-ways-to-access-pre-ipo-shares-11940509), that this will make it easier for investors to gain indirect exposure to the story of OpenAI’s pre-IPO shares through ETFs. That may amplify market attention, but it also draws OpenAI earlier into the valuation pressure and sentiment swings that resemble public-market scrutiny. Once a private company becomes central to a broad investment narrative, it must answer not only to enterprise clients and developers, but also to much wider expectations in the market.

On the surface, this latest release is another vote of confidence from capital markets in a star company. At a deeper level, however, it is really an attempt to answer a larger question: as AI moves from technical breakthrough to widespread deployment, who will truly control costs, command the entry points, integrate the ecosystem and turn highly unstable innovation rents into a stable industrial order? Seen that way, $122 billion is not an endpoint. It looks more like an entry ticket to the next arms race.

In the years ahead, whether OpenAI can preserve its lead will depend not only on whether the next generation of models is smarter, but also on whether it can sustain a tempo of compute expansion, product integration and commercial execution that competitors will struggle to replicate. America, China and Europe are offering different answers to the same question: will AI become a new monopolistic layer dominated by a handful of platform giants, or a more open, multipolar and functionally specialised global ecosystem? OpenAI’s fundraising announcement does not settle that question. But it does make one thing plain: this contest is no longer simply about who can build the best model. It is about who can construct the largest institutional system, the deepest infrastructure and the most indispensable point of entry.

Leave your name and email to receive future updates from our blog and product insights.

AI News | Editor: Sandy Google has moved artificial intelligence one step closer to the everyday act...

Read Article

Background This case features a dental clinic offering a wide range of services. The clinic already...

Read Article

【 AI News | Editor: Sandy】 Google’s newly released Gemini for Mac looks, at first glance, like a s...

Read Article

AI News | Editor: Sandy On April 16th 2026 Anthropic officially unveiled Claude Opus 4.7 and made it...

Read Article

AI News | Editor: Sandy Anthropic’s latest launch, Claude Code Routines, pushes AI coding tools from...

Read Article

AEO | Editor: Adda Lin AI Overviews Are Not Just a New Feature. They Change the Narrative Structure...

Read Article

AI Software | Editor: Sandy Flux AI is an all-in-one platform that combines AI image generation, ima...

Read Article

AI News | Editor: Sandy On April 10, Anthropic launched the beta version of “Claude for Word”, embed...

Read Article

In today’s increasingly competitive pet food market, many e-commerce brands face the same challenge:...

Read Article

AI News | Editor: Sandy The latest development surrounding Anthropic is not merely a product update....

Read Article

ChatGPT Applications | Edited by Jason Chen When organizations begin adopting generative AI, the fir...

Read Article

AI News | Editor: Sandy On April 8, 2026, Anthropic unveiled “Claude Managed Agents,” a release that...

Read Article

Opinion / In-depth Analysis | Editor: Sandy As generative artificial intelligence evolves from answe...

Read Article

AI News | Editor: Sandy In its latest announcement in April 2026 ( https://ai.meta.com/blog/introduc...

Read Article

ChatGPT Applications | Edited by Jason Chen In the age of social media dominance, Facebook (FB) has...

Read ArticlePimker - The AI marketing platform built for businesses

© Pimker 2026 The AI marketing platform built for businesses All rights reserved.